Not all markets are created equal, but they do share some features in common. Distilled to their most elemental components, markets tend to include a buyer, a seller, a good or service being sold, a corresponding monetary value, and a forum for exchange. And as economist and Nobel laureate George Akerlof noted, it’s information and trust that keep these market-making variables in sync.

In his paper “The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism,” Akerlof describes how, when one party knows far more about the quality of goods being traded than the other party, the market sustaining both parties risks total collapse.

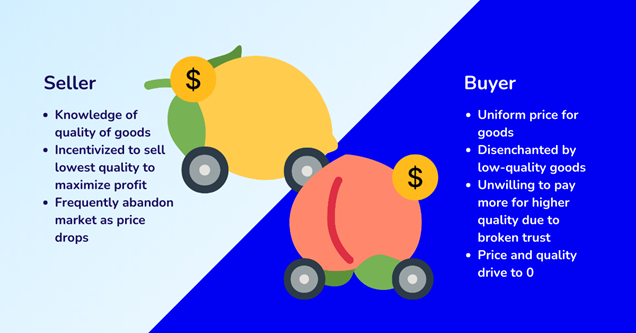

Akerlof cited the used car market (or a simplified version of it) to prove the effects of this dynamic, which he calls “informational asymmetry” — but he easily could have been talking about the specialty insurance ecosystem.

In Akerlof’s example, sellers know far more about their inventory than buyers do. If used car buyers pay a uniform price — since they don’t know which cars are good and which ones are bad — then sellers are incentivized to sell the worst cars, or the “lemons” of their lot.

That ploy works for sellers over the short term, as they have sold a car of sub-par value at a price well above what it actually deserves: a price and quality mismatch the buyer only recognizes once it’s too late. The discrepancy between what sellers and buyers know, however, dooms the market over time. As far more “lemons” get sold than “peaches” — good cars — buyers become less willing to blindly pay more to purchase good vehicles.

“It is quite possible to have the bad driving out the not-so-bad driving out the medium driving out the not-so-good driving out the good in such a sequence of events that no market exists at all,” he writes (without commas). As the average quality of cars traded decreases, so will price. This creates a negative feedback loop that drives prices and quality near zero.

Over time, we’ve seen how insurance markets are converging on these same existential risks. In some insurance markets, like health insurance, applicants often assess their own risks more effectively than insurance companies can. Adverse selection means “the average… condition of insurance applicants deteriorates as the price level rises — with the result that no insurance sales take place at any price,” Akerlof writes.

When its worst dynamics play out, the specialty insurance space can become a “market for lemons,” too. Imagine: A world in which MGA and risk capital providers alike fly blind relative to the dynamic loss prevention products they’re looking to underwrite and capitalize. Sound familiar?

Still, there is reason for optimism; there are ways to rescue markets, including insurance markets, from doom loops caused by unequal knowledge and the broken trust that comes thereafter.

In Akerlof’s eyes, private institutions can help drive “increases in welfare” by offering guarantees on goods sold, by creating brand differentiation among products, or by creating licensing systems that correspond to quality. These institutions work especially well when they distribute power to the stakeholders involved in the market, Akerlof argues, rather than ravenous concentrators of power.

Updating Akerlof’s arguments for the 21st century, we can also see the transparent collection and distribution of data as an obvious, invaluable rescue line for markets affected by informational asymmetry. In the case of insurance markets, underwriters can sell and maintain insurance products matching their clients’ risk, risk capital partners can add resilient and diversified products to their portfolios, and businesses can quickly obtain quality and sustainable insurance that matches the dynamic realities of their markets.

At Accelerant, we think of trust and transparent information as table stakes that can counteract the systemic dangers Akerlof fears. (And it so happens that they have a compounding benefit driven by network effects.)

In an ideal marketplace, as portfolios grow, more risk capital can flow to MGAs, improving their execution and thereby attracting more MGA Members, creating more data and a greater portfolio for risk capital partners. This virtuous cycle pushes the insurance landscape in more data-driven and informed directions — treating information as a binding agent and keystone for long-term success, rather than a resource to hoard for short-term wins.